Chart of the Month: April 2023

March Sadness: Assessing the Growth & Venture Landscape After a Tumultuous First Quarter

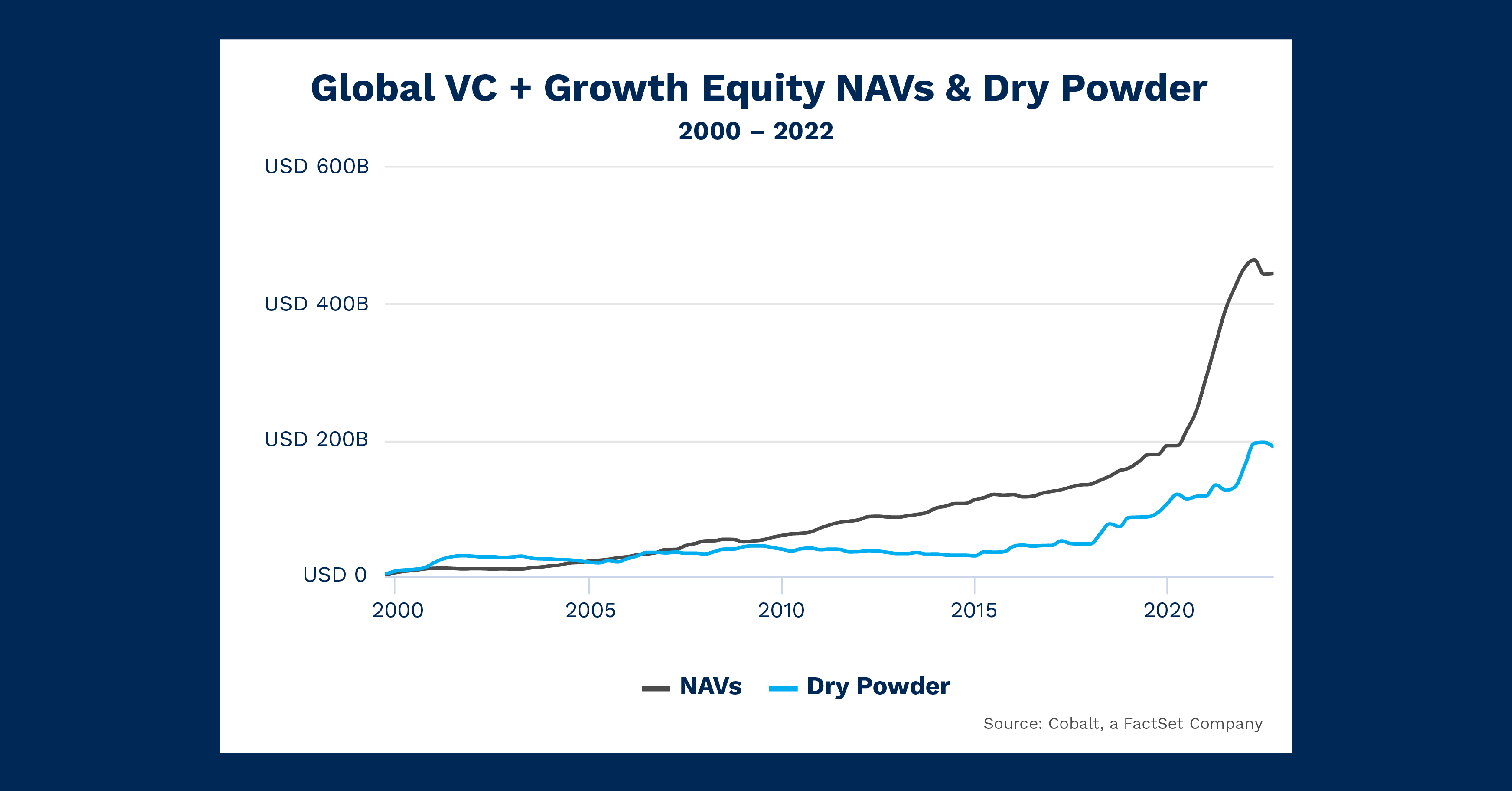

The first quarter of 2023 has come to a close, ending an impactful three months that sustained many different news cycles: rising interest rates, an equities rally, and most recently, the demise of Silicon Valley Bank (SVB) and its far-reaching implications. As we continue to assess the aftermath, we examined the state of venture capital and growth equity, spaces both closely associated with SVB. Today, we’ll investigate the net asset values (NAVs) and dry powder since 2000 of these two investment strategies, to see what lessons can be taken from the historical data.

Key Takeaways

The most striking aspect of the above chart is the dramatic rise in both NAVs and dry powder between mid-2020 and the end of 2021. Even compared to previous charts examining NAVs and dry powder in this time frame, the venture capital and growth space stands out. NAVs more than doubled in this time frame, from $215 billion to $460 billion, with dry powder experiencing a less dramatic but still significant increase as well ($115 billion – $195 billion).

The reasons behind this dramatic growth are mostly the same across the board: a low interest rate environment and historic amounts of capital being injected into the economy created an “everything rally” period for 2 years, which we see exhibited here. Venture and growth were particularly primed to capitalize even more than other strategies on this. Tech and quick growth, the main beneficiaries of the post-March 2020 period, are the focus of most of the space.

Looking Ahead

2022 and the beginning of this year were already creating an unwinding of sorts from the post-March 2020 frenzy in the markets. The instability in banking in both large institutions (e.g., SVB, Credit Suisse) and regional institutions has accentuated the uncertainty of the markets for the next few years.

For VC a growth, there’s a good argument to be made we will continue to see an unwinding in dry powder and NAV that have been exhibited the past few quarters. GPs may begin to act more cautiously with the portfolio companies they look at, potentially limiting performance upside. LPs may likewise look to de-risk their portfolios, which may cause a shift from the riskier end of private investments.

Subscribe to our blog:

Is There Geographic Bias in Macro Liquidity Trends in Private Markets?

Is There Geographic Bias in Macro Liquidity Trends in Private Markets? Building on our previous analysis of the role of…

Private Equity Performance: Large Strategies Versus Funds of Funds, Co-Investments, and Secondaries

Private Equity Performance: Large Strategies Versus Funds of Funds, Co-Investments, and Secondaries In private equity, the large strategies of buyouts,…

Examining Tariff Policy Impacts on Private Fund Contribution Rates

Examining Tariff Policy Impacts on Private Fund Contribution Rates Recently we examined the impact of Latin America presidential elections—which carry presumptions…